.avif)

It's Monday morning, and a regulator is on the line asking why last quarter's risk exposure report doesn't match the one filed three months ago. Nothing in the report logic changed. The trades didn't change. But somewhere between the booking system and the submission, a field quietly shifted meaning, and now a head of risk has to explain a number they can no longer defend. By the time anyone notices, the damage is already done: teams are arguing over whose definition is correct, reconciling differences by hand, and drafting an explanation for the regulator before the week is out.

After the 2008 financial crisis, regulators realized that these issues are system-level failures, not reporting failures, in how banks governed data as it moved from creation to decision-making.

BCBS 239 overcomes that gap by addressing the structural issues that make risk data unreliable when it matters most, not just by ensuring regulatory data compliance. In this way, it helps banks strengthen risk data so it holds up under real-world conditions as well as during reporting cycles.

What is BCBS 239?

BCBS 239 is a framework that defines how banks manage risk data across the organization by setting expectations for how banks govern, aggregate, and report risk data across a single, connected lifecycle. It also instructs on how to build in clear ownership, consistent data flows, and end-to-end traceability from the start. However, its primary objective is ultimately to keep risk data reliable as it moves from source systems into decision-making so figures remain explainable and consistent, even as conditions change and pressure increases.

Who BCBS 239 applies to

The Basel Committee on Banking Supervision introduced BCBS 239 after the global financial crisis, when many banks couldn’t explain their risk exposures quickly or consistently under pressure. Regulators initially applied the standard to global systemically important banks, then extended the same expectations to domestic systemically important banks as similar weaknesses appeared at national levels.

Today, supervisors across the EU, UK, and other jurisdictions use BCBS 239 as a benchmark for risk management, and many financial institutions beyond its scope have also adopted it to address ongoing data quality and data management issues.

The core objective of BCBS 239

BCBS 239 requires banks to build systems that can produce risk data on demand, not days later or with qualifications attached. That data must also tell the same story across reports and support senior management confidence, whether the business operates under normal conditions or faces periods of market stress.

Reaching that point, however, depends on how teams handle risk data day to day. In practice, teams need to understand the following aspects of risk data flows, ownership, and change:

- Knowing how risk data moves from one system to the next.

- Being clear about who owns critical data and who is accountable for it.

- Tracking how data changes as code transforms it across the lifecycle.

When a bank follows the BCBS 239 governance framework, it can explain its risk profile immediately instead of reconstructing it under pressure. That level of clarity supports supervisory review and gives leaders confidence that their decision-making reflects current conditions, not outdated reporting outputs.

BCBS 239 and RDARR

Banks often refer to risk data aggregation and risk reporting (RDARR) as the practical expression of BCBS 239. Once a bank can consistently produce risk data and explain how they derived it, RDARR then describes how the institution combines, presents, and updates that data as conditions change.

In practice, effective RDARR depends on these core capabilities:

- Risk data aggregation combines data from multiple systems without manual reconciliation.

- Consistent outputs deliver the same risk numbers across reports and teams.

- Explainability shows where figures come from and how the institution calculated them.

- Timely updates keep risk views current as markets or assumptions change.

However, problems arise when banks treat RDARR as a reporting task rather than a data production and data governance discipline. For instance, focusing on final outputs pushes their attention away from upstream processes where teams create, transform, and combine data. When those gaps persist, these same issues often repeat:

- Risk reports rely on manual reconciliation because source data doesn’t align.

- Identical risk questions produce different answers across teams.

- Small upstream changes break downstream reports without warning.

- Data quality issues surface late, often during regulatory submissions or periods of stress.

This means that over time, RDARR becomes a recurring clean-up exercise instead of a reliable way to understand how risk is evolving. But BCBS 239’s data management and governance practices address this issue by pushing controls upstream, keeping ownership clear, and preventing unreliable data from flowing into risk reporting practices unchecked.

The 14 BCBS 239 principles

BCBS 239 breaks down into 14 principles that work together as a system to describe what good risk data management looks like in practice across governance, risk data aggregation, and risk reporting.

One of the biggest frustrations with data governance and regulation is how abstract and process-driven the conversation gets. Endless frameworks, meetings, and policy documents that never quite reach the systems where the data actually lives. Here is what these 14 principles look like when they hit real workflows, real systems, and real decisions:

Governance and infrastructure principles

- Governance: Effective data governance in banks makes senior management directly accountable for risk data outcomes. This means leadership sets expectations, assigns ownership for critical data, and reviews whether governance practices hold up as data moves across systems rather than relying on policy documents alone.

- Data architecture and IT infrastructure: Risk data depends on a coherent data architecture and reliable IT infrastructure. However, risk data remains reliable only when systems share common definitions, support consistent integration, and allow teams to trace how data moves across business lines, legal entities, and regions.

These two principles exist because risk data problems rarely start at reporting time. Usually, they begin earlier, when accountability is unclear or systems can't support consistent data flows across the organization.

Citigroup is the clearest example. In October 2020, the OCC fined Citibank $400 million for what the regulator called a long-standing failure to establish an effective risk governance framework, data governance program, and supporting IT infrastructure.

Four years later, in July 2024, the OCC and Federal Reserve added another $135.6 million in penalties for insufficient progress on the same data management issues, bringing Citi's total to over half a billion dollars for governance and infrastructure gaps the bank still hadn't closed.

Risk data aggregation principles

- Accuracy and integrity: Risk data needs to remain accurate as it moves through systems. This requires shared definitions, documented transformation logic, validation rules, and escalation paths so issues surface early instead of compounding downstream.

- Completeness: A complete view of the risk profile requires capturing every material exposure across business lines, entities, and geographies. The trap is assuming downstream aggregation is what produces that completeness. Aggregation summarizes, and summarization hides what changed upstream. Completeness has to be enforced where data is produced, not reconstructed in the warehouse.

- Timeliness: During periods of market stress, supervisors and leaders need updated views quickly, not after manual reconciliation or delayed processing. Providing timely information instead allows risk data to support action when conditions change.

- Adaptability: Risk data processes that break under change create repeated remediation work and undermine confidence in reported results. That's why risk data systems need to instead adjust as products change, markets shift, and regulatory standards evolve.

These four principles focus on how banks produce risk data and combine it across systems in a way that remains reliable under pressure. These failures often surface during stress, but their root causes tend to appear in everyday data handling.

JPMorgan's 2012 London Whale incident is the textbook case. A Value-at-Risk model used to aggregate the bank's synthetic credit portfolio risk was rebuilt in a chain of Excel spreadsheets that required manual copy-paste between steps. One formula divided by the sum of two rates instead of their average, cutting reported risk roughly in half overnight.

Aggregated risk metrics also rolled the synthetic credit portfolio up under broader CIO-level exposures, drowning out the position's true size. The bank lost more than $6 billion before the aggregation errors were uncovered.

Risk reporting principles

- Accuracy in reporting: Reports need to reflect underlying data without distortion. Teams must also be able to explain how they produced reported numbers and trace them back to their data sources when questions arise.

- Comprehensiveness: Risk reports should cover all material risk areas and provide enough context to interpret results, rather than presenting isolated metrics without explanation.

- Clarity and usefulness: Risk reporting practices work best when they help leaders understand what changed, why it changed, and what further actions are necessary instead of forcing interpretation through follow-up analysis.

- Frequency: The reporting cadence needs to align with risk levels because, as volatility increases, reporting processes need to support more frequent updates without rebuilding reports.

- Distribution: Effective oversight requires risk data to reach the right audiences without distortion or delay. Reports need to remain accessible and consistent across leadership, risk teams, and supervisors.

Reporting quality depends on how closely reports connect to the underlying data and its transformations. This set of five expectations addresses how risk data becomes information that supports decision-making.

Credit Suisse's $5.5 billion loss on Archegos in March 2021 is what happens when these break down. The independent Paul, Weiss report found that risk reports systematically understated a single client's exposure, roughly $20 billion at the peak, because the bank's reporting framework couldn't surface the concentration in a form senior management could act on.

Limit breaches ran for an average of 47 days for active excesses and 100 days for passive ones, and stress scenario losses exceeded the entity's $800 million scenario limit by hundreds of millions without triggering escalation. The reports existed. They just didn't communicate the risk clearly enough or quickly enough to change the bank's behavior.

Supervisory review and cooperation

- Supervisory review: Supervisors assess whether banks can aggregate and report risk data on short notice, including during on-site or on-demand requests, rather than relying solely on periodic submissions.

- Remedial actions: When gaps emerge, supervisors expect clearly defined remedial actions with supporting timelines, ownership, and regular progress reports.

- Cooperation: For banks that operate across multiple jurisdictions, supervisory cooperation helps teams maintain consistent oversight and reduces the conflicting requirements that strain data processes.

These three requirements describe how regulators assess BCBS 239 compliance and respond when weaknesses appear by reflecting the expectation that risk data capabilities remain usable under scrutiny, not just during scheduled reviews.

The ECB's own track record shows what happens when banks can't meet that bar. After a 2016 thematic review found that none of 25 significant institutions had fully implemented BCBS 239, the ECB followed up in 2019 with a letter to all directly supervised banks demanding substantial improvements. By 2023, the Basel Committee's seventh progress report found compliance had barely moved. Only two of 31 global systemically important banks were fully compliant.

The ECB responded by publishing its Guide on effective risk data aggregation and risk reporting in May 2024 and signaling tougher remedial measures, including Pillar 2 capital add-ons, on-site inspections, and fines, for institutions still failing to comply.

Why BCBS 239 matters beyond regulatory compliance

In practice, BCBS 239 lands at most banks as a top-down mandate and a cost of doing business, which is why ten years in, only a handful of G-SIBs are fully compliant. The principles themselves are sound, but they do not take hold while the work is owned by a compliance program separated from the systems where risk data is produced.

The banks that close the gap move enforcement into those systems, so completeness, accuracy, and timeliness become properties of how data is created, not artifacts of how it is reported.

Here’s a breakdown of how that works:

Impact on risk management and decision-making

Leadership’s decision-making depends on their confidence in the numbers. When risk data arrives late, changes between reports, or lacks source traceability, for example, leadership will naturally spend more time questioning the data than acting on it. In fact, according to Deloitte’s 2024 BCBS 239 Benchmark Survey, while 68% of banks expect BCBS 239 to improve how leadership guides the business, only 21% report seeing that benefit in practice so far.

But the issue here isn’t awareness since most banks understand what BCBS 239 should enable. Rather, this gap opens when governance lives mainly in policy documents, data still moves through fragmented systems, and teams treat lineage only as something to document after the fact. In those conditions, risk data can appear complete at the reporting layer while remaining difficult to trace or explain beneath the surface.

However, when banks build governance, data flows, and lineage into their day-to-day operations, leaders spend less time defending numbers and more time acting on them. As a result, decisions move faster because the data behind them holds up under scrutiny.

The consequences of weak compliance

When BCBS 239 implementation falls short, supervisory attention increases. The repeated reviews, ongoing progress reporting, and extended remediation programs that result then pull time and resources away from risk, data, IT, and compliance teams. In some cases, weak progress even leads to heightened supervision, capital add-ons, or third-party reviews, which all increase cost and distract leadership from strategic priorities.

Inside the bank, the effects surface every reporting cycle. Teams patch data issues late, reconcile figures manually, and scramble to explain changes that upstream system updates caused. And over time, risk discussions will focus less on exposures and more on defending reporting outputs.

BCBS 239 as a foundation for other regulatory standards

Strong BCBS 239 practices extend beyond a single regulation because they connect governance, data flows, and lineage across the risk data lifecycle. This governed, traceable risk data supports regulatory reporting more broadly and reduces duplicated effort across financial services teams.

That same connected foundation also makes it easier to absorb new supervisory measures. Because banks already understand how risk data moves, changes, and holds up across systems, new requirements build on existing capabilities instead of triggering one-off remediation efforts.

The EU's Digital Operational Resilience Act (DORA), which became applicable on January 17, 2025, is the clearest example. Its requirements for ICT risk management, incident reporting, resilience testing, and third-party oversight sit directly on top of the data architecture, traceability, and governance capabilities BCBS 239 already expects. Banks that built those capabilities as policy documents now face a second regulatory test of the same systems. Banks that built them into how data is produced absorb DORA as an extension of the work, not a parallel program.

Best practices for BCBS 239 compliance

Strong BCBS 239 programs don’t rely on audit-time fixes or last-minute remediation. They instead hold up because teams design their data practices to scale, remain explainable, and continue working as systems change. But that shift requires treating governance, data flows, and lineage as operational capabilities, not just documentation tasks.

The best practices below reflect how banks move from surface-level compliance to systems that support BCBS 239 on an ongoing basis:

Treat risk data as a system

When banks focus only on final reports, they miss where problems begin, like small differences in definitions, transformation logic, or ownership. These issues appear upstream and often remain invisible until looking closer via audits. This means teams have to spend time reconciling results instead of understanding how risk has changed.

A more effective approach treats risk data as an operational system that spans creation, transformation, aggregation, and reporting. But that system requires clear structure, ownership, and visibility as data moves across it. In practice, this means establishing a consistent operating model for risk data that includes this information:

- Shared definitions for risk metrics across teams and reporting processes

- Ownership at the point where data enters and changes, not only at reporting time

- Visible data flows between systems as part of normal operations

- Sources for surfaced issues so teams don't have to patch them downstream

Managing risk data in this way aligns risk, finance, and compliance around the same definitions and responsibilities. Reconciliation work drops as a result, and data also remains consistent from one run to the next.

Build end-to-end traceability into data architecture

BCBS 239 expects banks to explain where the numbers come from and how they change over time. But that expectation breaks down when data lineage exists only as static documentation that teams update periodically.

Programs that scale instead embed traceability directly into the data architecture. That way, as systems evolve, lineage updates alongside them. And when products launch, logic changes, or data sources shift, traceability remains current because it accurately reflects how data moves through the environment.

This end-to-end visibility supports supervisory questions without forcing teams to reconstruct history under pressure. It also makes on-demand reporting possible when conditions change because teams can trace figures back through transformations instead of reverse-engineering results.

Automate validation, lineage, and governance

Manual controls create recurring risk because they sit outside the systems that produce and transform risk data. Additionally, solutions like spreadsheets and point-in-time checks may fix an issue for one reporting cycle, but they ultimately don’t change the underlying data processes. Later on, as sources update or logic changes, those fixes will inevitably fall out of date, and the same data quality issues will return.

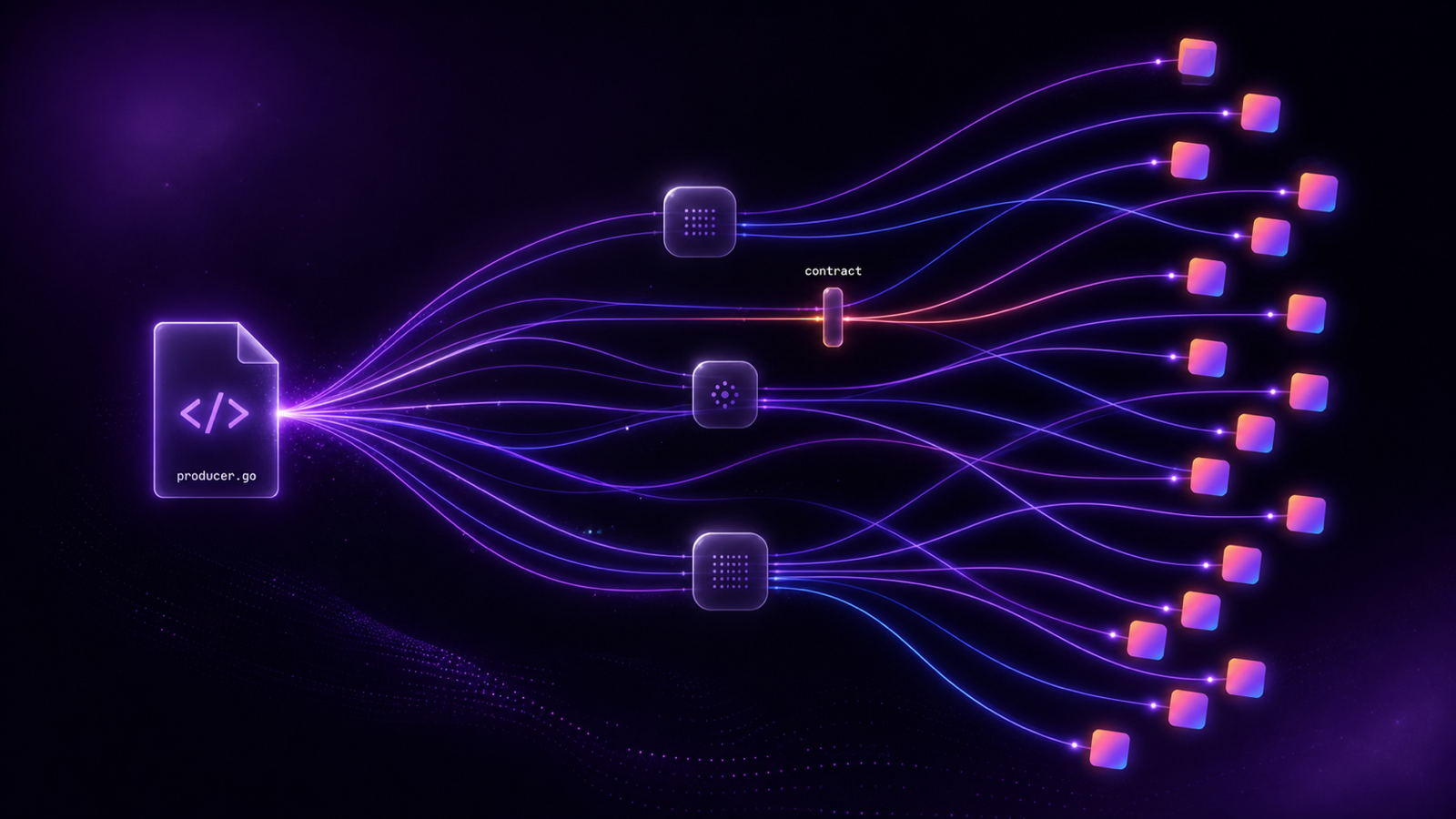

Modern tooling closes that gap with data contracts: a producer and consumer agree, in code, on the schema, semantics, constraints, and ownership of a critical data asset, and that contract becomes the enforcement point. When a developer's pull request changes a field that risk reporting depends on, contract checks run in CI/CD and surface the violation before the change ships, not after risk numbers move. Lineage and validation update alongside the code, so completeness and accuracy live in the systems that produce data rather than in policy documents.

Gable applies this model to risk data by putting data contracts on the assets that feed risk reporting. Contract checks run in CI/CD whenever a producer changes upstream code, so backwards-incompatible changes are caught before they reach downstream risk calculations. Ownership, traceability, and validation are encoded in the contract itself, which is how risk data stays explainable and audit-ready as systems evolve.

Over time, these efforts reduce repeated clean-up work and shift effort toward using risk data rather than defending it. And while automation doesn’t replace governance decisions, it does make them enforceable at scale and auditable under supervisory scrutiny.

From BCBS 239 compliance to confident risk data

BCBS 239 provides a framework for how banks govern and understand risk data as it moves across the organization. At its core, it sets expectations for governance, system-wide data flows, and traceability so risk data remains reliable under change and scrutiny.

But meeting those expectations requires more than passing reviews. When banks build strong data foundations into daily operations, they also reduce recurring remediation, improve visibility into how they produce data, and gain confidence that decisions reflect current conditions rather than reconciled outputs.

Gable supports this shift by helping banks operationalize BCBS 239 at scale. By embedding traceability, validation, and governance directly into data workflows, Gable makes risk data explainable and audit-ready as systems evolve.

See how Gable works to make BCBS 239 adherence a day-to-day capability of the systems that produce risk data, not a periodic compliance exercise.

Gable

May 13, 2026

.avif)

.avif)